As I walk to work every day I pass a series of “Payday lenders”. These companies offer an advance to individuals without cash at a high interest rate, which is implied in the “fee” for providing cash as well as the short duration of the loan (a couple of weeks or a month). These practices are often frowned upon in the media as “taking advantage” of the poor.

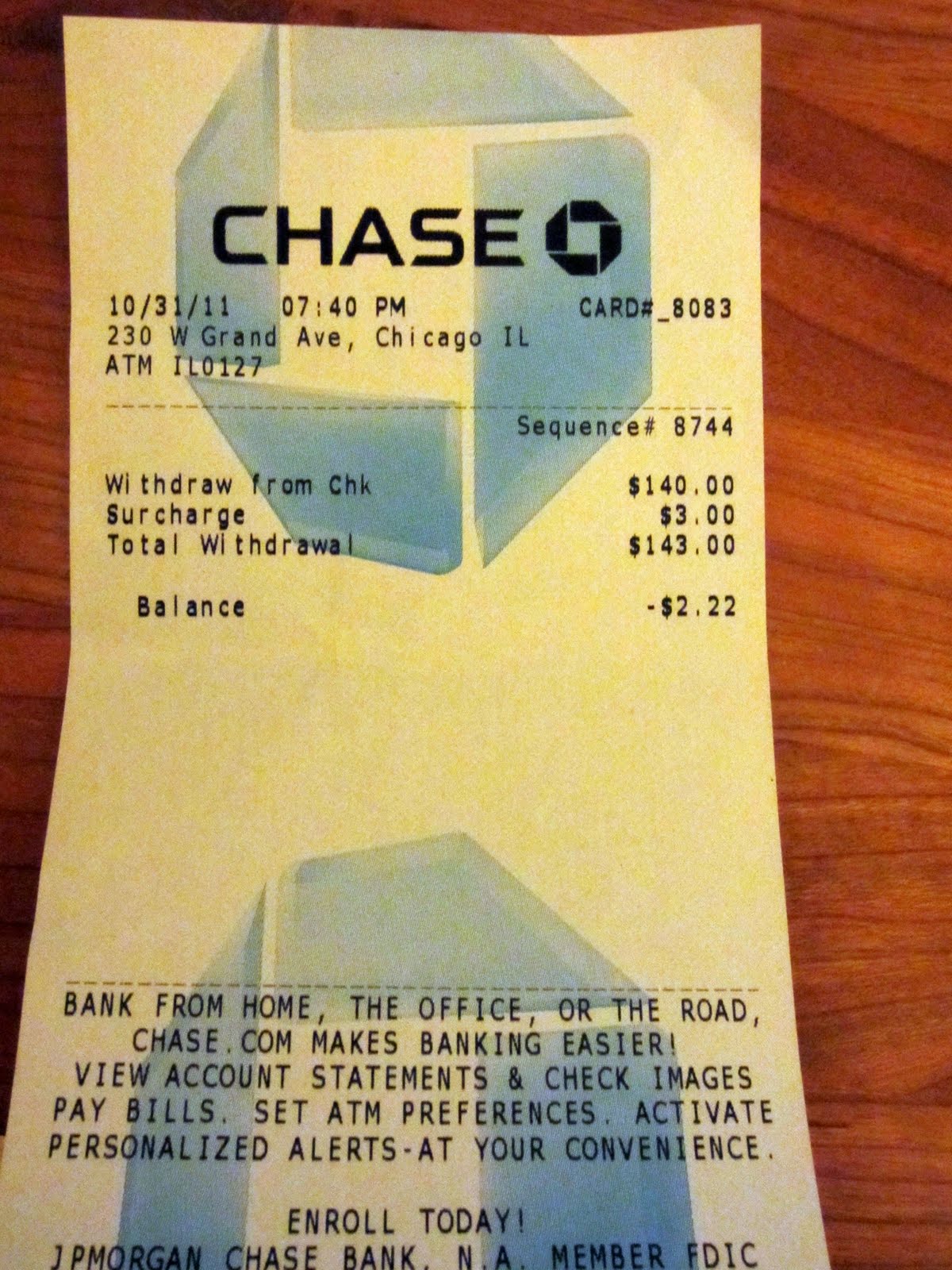

As I pulled cash from an ATM I had to pull out the receipt of the prior person at the cash station (they had already left long ago) in order to get at my receipt because they just left it in the ATM. You can see the receipt below (it didn’t have any identifying information).

This person is not someone who should be banking at all. They had a balance of $141 or so in their account, but they withdrew $140 with a $3 fee for using an out-of-network ATM, meaning that they were now going negative in their account. I don’t know what bank they use (it isn’t Chase) but many of these banks charge $20 or $30 or more for every single overdraft. Thus the “true” cost of pulling out this cash is really $3 out of network fee plus the $30 or so overdraft fee. This is a huge cost as a percentage of the money withdrawn ($33 / $140) = 23%, and if you assume any sort of “time” in order to compare it to a loan such as you’d get for a payday then it is astronomical. Let’s assume 1 month duration and that it isn’t APR just straight interest then let’s multiply by 12 and you get 276%. Under any sort of “compounding” model it would be much higher.

The wikipedia entry under “payday loan” is surprisingly balanced, given that the industry has an overwhelmingly negative connotation in most media.

Payday lenders do not compare their interest rates to those of mainstream lenders. Instead, they compare their fees to the overdraft, late payment, and penalty fees that will be incurred if the customer is unable to secure any credit whatsoever. The lenders therefore list a different set of alternatives (costs expressed here as APRs for two-week terms)

$100 payday advance with $15 fee = 391% APR;

$100 bounced check with $48 NSF/merchant fees = 1,251% APR;

$100 credit card balance with $26 late fee = 678% APR;

$100 utility bill with $50 late/reconnect fees = 1,304% APR.

The banks too prey upon those who are low income or (relatively) financially illiterate; the fees by transaction can add up very quickly even for a small account. As a percentage of the account or if any sort of “time” basis is factored in, the results can be significant.

While I am not an expert in the system and don’t know all of the alternatives it seems obvious that giving people access to credit, the immediate ability to withdraw cash, and not limiting their ability to accrue fines and fees is a sort of recipe for disaster. The person who withdrew this sum from the ATM, for certain, isn’t the type of person who is going to fare well in a modern banking system.

Cross posted at LITGM

I have wondered what the fee (or is viggerish a more appropriate term?) for those “check cashing” places – I would suspect the people using them don’t care. And it isn’t just the poor – many people when buying a car are only interested in “how much a month” – not considering they could easily pay an amt approaching the purchase price of the car if the loan is stretched out enough.

My father has a good saying – “You are only going to make so much money in your life. How much of that do you want to spend in interest?”

Equally as bad, or maybe worse in some instances, are the automobile title-loan establishments. I’m familiar with one particular person who received a $600.00 loan against their title, paid back over $2000.00, could not make the next-to-last payment, then renewed the loan and started the whole miserable process over again. She ended up repaying over $5000.00 for a $600.00 loan.

Michael – that rate would make the Mafia embarrassed…..

I don’t think I could work for one of those places….Wouldn’t you want to tell your friend “$2,000 is more than enough”?

…whoops, I mean Barry – I wish we had the ability to edit these posts…..

“… is a sort of recipe for disaster.” Disaster for them, windfall for the banks. It is no accident. There are a ton of ways to rip off poor and ignorant people and America’s businesses are working as many of them as they can. It is a national disgrace.

There’s a sucker born every minute. “For every credibility gap there is a gullibility fill”.

This type of abuse could be resolved with a few minor changes to the law. We should do it.

Before jumping on the payday lenders, consider the business, the market, and the customers.

The business in making short duration loans. The maximum value is usually limited by law. (In Michigan I think it’s $750, from all lenders.)

The market is anyone who needs cash immediately. These are usually people at the lowest income levels, subsisting on minimum wage one major problem away from financial catastrophe – e.g. an “unplanned” root canal.

The customers are people locked out of the traditional banking system.

Strange as it may seem, you can not simply walk into a bank and open an account. They run a credit check, now. And they may reject you if your circumstances aren’t right. e.g. bad credit and low paying new job. You could even be rejected because you don’t have enough income. In this economy, that could be anyone.

The rates/fees are horrible – unless you look at the alternative (as Carl does). Talk about shutting them down is fine – but recognize that for the people who use them, there is no alternative.

Lex – you can legislate some laws but the unscrupulous will always find a way around them. And what John W. says is also true – loans are priced according to risk. In most cases – Barry’s example of the woman paying $5,000 for a $600 (secured) loan – well on the one hand it was her choice but on the other hand the lender had a secured asset to seize if the loan fell through. I don’t understand the mafia-like rates on that loan. Reminds me of the scene in Goodfellas where the 2 hoods are beating up the business owner for being late on the “viggerish”.

In CA the well intentioned legislators thought they would eliminate unscrupulous auto shop owners by requiring written estimates before leaving your car at a shop.

Well, the dishonest shops will give you an estimate – really jack up the cost – and the customer still signs the estimate. Or they call you later saying “I didn’t think the gizwidgit would be bad but it is – and it’s another $2,000”. So you still rely on the integrity of the shop owner (and the good ones get all the business they can handle – again – the market working)

So you can’t legislate laws that make dishonest people become honest.

In my younger days I used to get upset if a business I had been using raised their prices such that I didn’t want to pay. But bottom line its a business offering a product or service for the price they want and there are potential consumers who can pay the price – or not – by choice. Some pay and some don’t.

Out here we have this chain called “Rent A Center” – where you can pay an exorbitant fee to rent a TV, computer, what have you.

They cater to people who have lousy credit I suppose – otherwise how can you explain a person “renting” a computer that will be paid off in a matter of a few months with the high rent.

But that person doesn’t have to have that computer. Used ones are so cheap as to be considered disposable. Its their choice. In many cases – maybe most – the poor are poor because of their life habits. If you have good habits you don’t stay poor.

But in the case of the woman Barry knows – if I were the lender I would be ashamed –

years ago when I had a business we had an employee who was paid well but got into trouble with the credit card companies. A rare story, I know.

But he would get calls all day from bill collectors.

If you have to have it now – even if you can’t afford it – you get in to trouble.

it’s that simple.

Bill (incognito)

We already have legislation. It’s called Dodd-Frank. It makes these problems worse by driving up banks’ costs. The banks pass the costs to customers. As always, poorer and less savvy customers get hit with the brunt of the charges. Cut regulation and banks’ costs will decrease and they will have more incentive to compete for the business of people who now use more-expensive non-bank alternatives.

The payday loan companies fill a need. They are competitive. There is a reason why none of them dramatically undercuts the others on rates. It’s that their customers are bad credit risks. (It may also be that they are overregulated by local govts who restrict entry into the market, but if so that supports my argument.) Regulate them more and they will have to increase their rates or be more selective about their customers. You can’t legislate financial responsibility. For people with little money or bad credit histories, the alternative to payday loan companies isn’t banks, it’s loan sharks.

I agree with Jonathan, about the realistic alternative to payday loan places. My daughter had a brief go-round with a bank, which left her without a viable account, so she was dependent for a while on a payday loan/check-cashing place, which charged a relatively small fee for cashing checks from her occasional employers. They did serve a very useful function in that they offered a a debit card, which her cash could then be loaded onto. She rather preferred that arrangement, after that very bruising encounter (tale too long to tell) with a bank which appeared to enthusiastically pile on the overdraft fees. If there was no balance on her pre-paid card – it would be refused, flat-out. For her, it provided the same service as a bank, for only slightly more in fees.

I went through a frustrating experience with my daughter when she was a college freshman. I gave her a debit card. She would charge $1.20 over her balance and get a $35 fee. I went to the bank and tried to get them to simply refuse credit in such a case. They would not. It was very frustrating. Fortunately, she is more responsible not. It did not make me fond of the back.

One thing I read years ago about the banks – is because their traditional means of making money – loans – is now done by so much competition – they are having to resort to “creative” ways of getting income.

The strangest thing I have heard was their desire to charge $5 for a debit card – taking out your money instantly (as opposed to using the float – their money – on a credit card).

But $35 for a $1.20 overdraft? That has to be a simple computer setting the bank has to accept – or reject – the transaction.

Jonathan,

Blaming it on Dodd-Frank is certainly the banker’s story.

I suspect the Gramm–Leach–Bliley Act in 1999 that repealed the prohibitions in the Glass-Steagall Act that put a barrier between investment banking and commercial banking is more to blame. Once that happened the local banks became local no more – just grist mills for cash to fund the more profitable investment banking side. When banks had to be profitable by servicing customers and making sound loans they took pretty good care of small customers. When small customers are perceived as a nuisance that distract the bank from the real profits tobe made in investment banking, slapping $35 charges on the $1.20 overdraft Michael described became the norm. If Michael’s daughter doesn’t like it she can lump it – the bank doesn’t care because anyone with an overdraft isn’t the sort of customer who fuels their investment banking busines – so who needs ’em?

There are different kinds of banks that serve different clienteles. People with money always have alternatives. Regulation raises the cost of doing business and prices some banking options out of the reach of poor people. Then do-gooders notice that poor people have few alternatives, blame the service providers who actually do cater to the poor, and propose additional regulations that further increase costs and eventually make the problem worse.

“$35 for a $1.20 overdraft?” A scam. Like the huge charges on ATMs. The industry is parasitic at this point. Charging several thousand dollars in fees and interest on a few hundred dollar “loan” made to poor and unsophisticated people, as routinely happens, is not beyond the reach of reasonable legal limitation.

Consumers are better protected by competition than by having legislators and bureaucrats telling banks how to do business. Many if not most of the ATM and other fees that people are complaining about were introduced after Dodd-Frank and perhaps other poorly conceived rules limited the ways in which banks could earn money. But sure, pass more rules to protect people. Then the marginal customers will be priced out of banks and into currency exchanges and other higher-cost bank alternatives. Then crack down on the currency exchanges and payday loan companies and you will price the marginal customer out of all legal alternatives.

If your bank charges $35 for a $1 overdraft then switch banks. If you find that other banks charge similar overdraft fees then there might be a good reason for it. For example, low-income customers might value having an emergency option to overdraw their checking accounts for a price. I don’t know; it’s an empirical question. My bank was eager to offer me overdraft coverage, I assume because they wanted to earn fees. I declined but someone else might want the option. Problems arise when third parties, who can’t possibly understand all of the issues, tell banks how to do business. These are often the same third parties who crashed the economy by mismanaging the Fed and by forcing banks to write mortgages to people with bad credit.

There should be fewer banking laws and regulations, not more.

Unregulated banks? Sounds like the S&L’s of the 80’s writ large and we saw how that worked out.

But no regulation means no FDIC insurance and absolutely no TARP. They fail then they fail and their depositors go down with them … which means many of them would not be around today to complain about being over-regulated… but if the government (which means us) is going to back them up then they have to play by the government’s (the taxpayer/citizen/customer) rules … fair is fair, right Jonathan?

“Consumers are better protected by competition.” But what they face is collusion. It is not a matter of more or less regulation, it is a matter of what and how.

I’m from Australia but lived in the USA for nearly two years during the dot-com thingo (eventually company ran into trouble and with my visa no longer valid I went home).

It really struck me how lousy the American banking system is. Firstly, many banks there don’t seem to be national. Here all the big banks have branches in all states and cities. Also, fees here are much more reasonable.

If you try to overcharge your debit card here it’s just refused. Worst case if you do overdraw they’ll just charge you interest on the balance, so if the overdraft is small you don’t pay much. Also we don’t have stupid restrictions on how often you can draw money from a savings account. So I keep my money in a savings account and transfer it to another account which is linked to a debit card when I want to spend it. That way nobody can charge my card more than I am expecting.

Bank-to-bank transfers here are so easy and convenient that most online stores accept bank transfers for payment of items (usually, along with debit/credit cards, PayPal etc.). I remember that being much more difficult in the USA.

Opening an account here is quite easy. Much easier than it was for me to open one there. That was a painful process.

Overall I don’t understand why your banking system is so user-unfriendly.

Overall I don’t understand why your banking system is so user-unfriendly.

There seems to be a bias towards poor management and poor service. I don’t know why this is true but it is.

Personally, I think the recent increases in fees are probably tied more to historically low interest rates than anything else. Checking accounts have costs, which would typically be at least partly covered by the spread between a interest rates on the account vs a passbook savings account or short term CD. (Yes you used to be able to get interest on a checking account balance). With short term rates almost at zero, this spread has vanished, so the banks need to come up with other revenue streams to recover the lost spread (along with cutting costs by limiting “free” services). I suspect the simple approach of just charging $25 a year or so as a flat fee is ruled out by unwillingness of customers to “pay” for what they are used to getting for “free”.

It always surprises me how often people fail to consider the impact of the interest rate environment on financial activities. As another example, one of the driving forces behind the expansion of credit card offerings over the last 30 years has been the decline in interest rates. Since most states have maximum interest rate laws (18% used to be pretty standard), when regular secured credit rates are 13-15%, like they were in the early 80s, credit cards were only offered to the most credit-worthy customers because the available risk premium was relatively small. Store cards serviced customers at the margins, trading off sales for higher risk than a 3rd party lender would accept. As overall rates declined, the spread increased and the banks could then profitably offer unsecured credit to riskier customers. Pure store cards have largely vanished (replaced by Visa/MC with store rewards) because there really aren’t any valuable customers left who need them.

Phwest..”Checking accounts have costs, which would typically be at least partly covered by the spread between a interest rates on the account vs a passbook savings account or short term CD. (Yes you used to be able to get interest on a checking account balance). With short term rates almost at zero, this spread has vanished”

But checking accounts, savings accounts, and CDs are all *sources* of funds to the bank…the relevant “spread” here is that between the bank’s cost of funds and the return it can get on loans.

“But checking accounts, savings accounts, and CDs are all *sources* of funds to the bank”¦the relevant “spread” here is that between the bank’s cost of funds and the return it can get on loans.”

True… as I understand it, part of the problem now is that banks can’t make loans. The reasons seem to be the combination of: excessive regulations which either limit the loans they can make or prohibit charging interest rates consummate with risk, and the poor economy driving down the demand for credit. A lot of companies are sitting on cash that they can’t do anything with; they don’t need to borrow more. Homeowners obviously aren’t buying, and the people who do need money (e.g., the unemployed) aren’t credit-worthy.

So what’s happening is that banks are devolving into money warehouses. Your money in the bank is not productive, it’ just taking up space (in terms of the bank’s mandatory minimum reserves), and it actually represents a cost to the bank. As Johnathan points out, the wealthy will always have alternatives; in this case it’s the recent rise of private banks to which membership is restricted to invited wealthy depositors. These non-bank banks, freed of a lot of regulation, can loan and invest money profitably, while banks that serve the public cannot. You know the story: the rich get richer etc. And it isn’t just the poor who lose out; a lot of the middle class has no productive place to invest their money either.

So yes, things like Dodd-Frank are achieving the exact opposite of what they claim to achieve. And if Chris Dodd or Barney Frank were to speak with you honestly on the matter, they’d tell you that they’re fine with that.

One thing I’ve learned the hard way is not judge another person’s business when I know nothing about the internals of that business. Banks are one of those institutions that every thinks they understand because they deal with them so much but the vast majority of us never see what goes on behind the scenes. I very much doubt any of us really understand why banks do what they do in any particular circumstance.

I used to know a guy that spent a stint doing programming for banking software he had some stories. Beyond the baroque security precautions e.g. no single programmer can work on all parts of a unit of code, the regularity and accounting constraints were enormous. He said just learning the specialized nomenclature took him weeks.

Things like overdraft protection might seem simple but from an accounting perspective, it easy to see how they could get complicated in a hurry. If a bank fronts you a dollar overdraft, in accounting terms they’ve loaned you a dollar and they have to book that dollar. That suddenly creates a new accounting category that has to managed. If they decide to have free overdraft protection up to $20, they’ve now have to set money aside to cover all that and for banks, money that isn’t making interest is a loss (usually, because banks don’t have money of their own but are lending money they themselves borrowed at interest from depositors.) Besides, we all know that if most people think they have $10 free overdraft protection, then they mentally add $10 to their account and -$10 becomes the new zero and the whole thing starts all over again.

Bill Waddell,

Unregulated banks? Sounds like the S&L’s of the 80”²s writ large and we saw how that worked out.

S&Ls were never “unregulated”. S&L’s were a creation of the federal government. They were intended to form pool of money from middle-class workers for local housing lending. They had their own custom rules and regulations other forms of banks did not.

S&Ls were said to work on the 3-6-3 model, “Borrow at 3%, loan at 6% be on the golf course by 3pm.” This worked okay for 30 years until the Federal Reserve began inflating the currency in 1967. By the late 70s we had 14% inflation and the S&L industry was trying to 8% or more to depositors with money from 6% mortgage repayments. The S&Ls began to implode. The inexpensive but long term mortgages they had relied on had been rendered almost worthless by inflation.

The “deregulation” of the early 80s was an attempt to link S&Ls together with other financial institutions that could somehow ride out the inflation. It didn’t work. The S&Ls were to far gone by that time. Instead of lashing together a lot of small boats to make one big seaworthy raft, they ended up lashing boats that float on their own to those that were already anchors headed for the bottom.

The S&Ls were just like Freddie and Fannie today. They seemed like they could do better than the free market but in reality, they just displaced the true cost cheap mortgages into the future. If it hadn’t been inflation it would have been the decline of property values in the northeast. They were just to inflexible to survive long term.

Cousin Dave…there seems to be a considerable demand for business loans that is not being satisfied by banks. This is a factor in the growth of Business Development Companies, which obtain the money they loan out not from depositors but from shareholders, bondholders, and the cash flow from repayment of past loans. (Some of them also take an equity kicker, typically in the form of warrants.) They do not have the advantage that banks have of super-low cost of funds, but make up for this, IMO, by being generally less-regulated and more entrepreneurial.

I think this is an interesting category of companies, and am an investor in several of them.

“It is not a matter of more or less regulation, it is a matter of what and how.”

Except that politicians don’t have a clue about what or how, nor are they ever likely to.

Any regulation that goes beyond punishing overt fraud and strays into issues of fairness or ethics is always going to have secondary consequences that completely swamp its intended benefits. Those who want to make a quick buck off of financially naive or desperate customers will continue to find ways to do so, and genuine innovators will be hampered.

History has proven this so many times I shouldn’t even have to point it out, at least not on this blog.