Yesterday I attended the Wisconsin Economic Forecast Luncheon. I was invited by a financial institution that I work with, who had a table reserved. The purpose of the meeting was to network, and to hear speakers talk about the forecast for the future as far as business goes. I would guess that there were about 500 people there representing all types of business across Wisconsin. There were lawyers, bankers, construction company owners, and many other business represented. Also attending were mayors of some cities, and many state representatives and senators.

Economics & Finance

Job Creation

Politicians, from Barack Obama on down, are spending a lot of time talking about “job creation.” Businesses, labor groups, and “experts” of various kinds are getting into the fun, each emphasizing that their proposed project W will create X jobs within Y time frame at a cost to the government of only Z.

I know a way to create at least a million jobs, almost immediately, at no government expense whatsoever.

Why California is No Longer a Paradise

People are leaving California and the once golden land has begun to decay. [h/t Intapundit] What happened?

“We’ve lived off the investments our parents made in the ’50s and ’60s for a long time,” says Tim Hodson, director of the Center for California Studies at California State University, Sacramento. “We’re somewhat in the position of a Rust Belt state in the 1970s.”

California has followed the grim path of the Great Lakes states.

Stock Selection

In the “efficient markets” hypothesis, all available information is factored into the stock price, making attempts to “beat the market” by selecting your own stocks a fool’s errand. Index funds, which were originally stock mutual funds, such as those at Vanguard, not only attempt to mimic rather than beat the index, they also sport much lower expenses. Thus even if the performance was the same for an index as a stock picker, the index would win with costs as low as 0.2% / year as opposed to 1% – 2% / year for managed funds. One advantage that remained of a stock selection methodology over mutual funds was related to taxes – individual stocks were definitely more tax efficient if handled correctly; now index ETF’s have erased that lead.

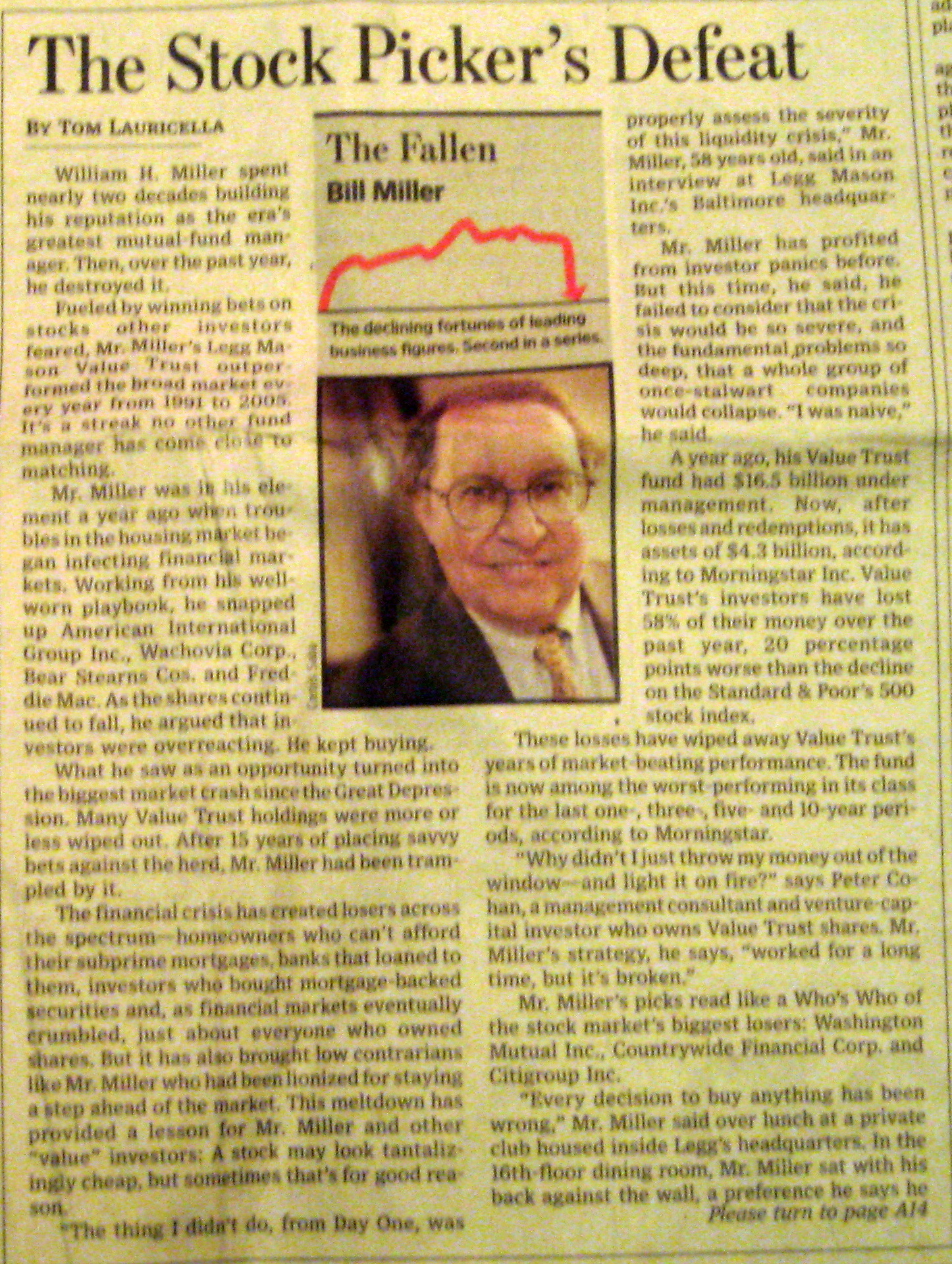

Of course, theories don’t always work in the real world, as the recent financial meltdown attests, when AAA rated financial instruments took significant losses. In a similar vein, those in favor of active stock selection could always point to a few candidates to make their cases. One candidate was Bill Miller, head of the Legg Mason Value Trust, who beat the S&P 500 for 15 consecutive years.

While Bill Miller may have been the “poster boy” for those that point to active stock pickers, he was a reticent candidate. He even said that a lot of his “streak” was due to timing on the calendar and didn’t strut around like a world-beater. Thus I didn’t take much pleasure in the this article…

Bill Miller, whose Legg Mason Value Trust achieved the unlikely feat of beating the S&P 500-stock index for 15 consecutive years, has become the fund world’s punching bag. So far this year, the fund is down a devastating 56 percent on account of bad bets on stocks including AIG, Washington Mutual, and Freddie Mac. This horrific year (combined with lackluster results in 2006 and 2007) has banished Legg Mason’s crown jewel to the ranks of the worst-performing mutual funds not only for the year, but for all standard periods of measurement.

An Odd(?) Recommendation

I am usually loathe to recommend anything remotely related to the NY Times or even link there*, but the Freakonomics Blog is very good reading, and the comments are usually very civil, intelligent and interesting.

*My main reasons are the terrible editorial pages and the fact that they will not renounce the Duranty Pulitzer.