Some Chicago Boyz know each other from student days at the University of Chicago. Others are Chicago boys in spirit. The blog name is also intended as a good-humored gesture of admiration for distinguished Chicago School economists and fellow travelers.

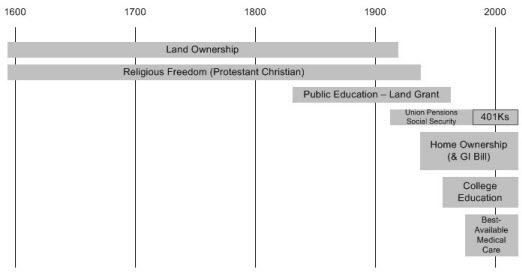

As someone who’s written several times (here and here) about the course of modern health care (its inherent complexity and cost), I’ve been watching the latest moves in US health care funding with a great deal of interest.

From the introduction of antibiotics to the breakthroughs in transplant surgery, medicine in the 20th century was in a position to provide dramatic improvements in health care (both quality of life and length of life) at relatively modest cost. Many consider it a golden age in medicine. My personal belief is that medical care is about to hit another burst of creativity and success (but at much higher cost-to-benefit) as non-invasive imaging, micro-surgery, diagnostic testing, and DNA-propelled pharmaceutical customizations kick in. I may be wrong, but I think my beliefs are a reasonable extrapolation of the trends in medical care since the end of the 1970s “silver bullet” period of medicine.

So what do my guesses about modern medicine mean in a new era of greater tax subsidies for US health care? An era which, by necessity, must politicize health care further. It got me to thinking about the hidden subsidies during earlier periods of American history, powered by the domestic political systems of the time, and driven by citizen/voter appetites. And it got me thinking about the law of unintended consequences.

After a few minutes scribbling on the back of an envelope, I came up with the following:

We have a little time left

The wise doctor said

Unless there’s a miracle

Which is another man’s trade

Selfish as always

I’ve started missing you now

Want to say so

Don’t know how

Want to hug you

Don’t know if I should

Hope you understand

I’d take your place if I could

In 1942, at the age of 22, Leo Marks joined the secret British agency known as Special Operations Executive, and soon became the organization’s Codemaster, responsible for the security of communications with SOE’s resistance and sabotage agents in occupied Europe. He usually briefed these agents…soon-to-be-legendary individuals like Violette Szabo and Forest Yeo-Thomas…before their departures and they all left indelible impressions on him. His memoir is a very emotional book: frequently heartbreaking, sometimes very funny. There is a lot about the technical aspects of cryptography, but these sections can be skipped or skimmed by those who are primarily interested in the powerful human story. Poetry, much of it written by Marks himself, played an important part in SOE’s cryptographic operations and hence plays an important role in this book.

Have retroactive predictability imposed on them through the foresight of 20/20 hindsight.

Taleb frequently points to the outbreak of World War I as an example of a black swan. He scoffs at historical accounts that present the outbreak as the result of trends that built up over the preceding decades, dismissing them as manifestations of the narrative fallacy:

Narrative fallacy: our need to fit a story or pattern to a series of connected or disconnected facts.

…historians arrive on the scene. They are the scholars who specialize in the study of “fat tail” events—the low-frequency, high-impact moments that inhabit the tails of probability distributions, such as wars, revolutions, financial crashes, and imperial collapses. But historians often misunderstand complexity in decoding these events. They are trained to explain calamity in terms of long-term causes, often dating back decades. This is what Nassim Taleb rightly condemned in The Black Swan as “the narrative fallacy”: the construction of psychologically satisfying stories on the principle of post hoc, ergo propter hoc.

Drawing casual inferences about causation is an age-old habit. Take World War I. A huge war breaks out in the summer of 1914, to the great surprise of nearly everyone. Before long, historians have devised a story line commensurate with the disaster: a treaty governing the neutrality of Belgium that was signed in 1839, the waning of Ottoman power in the Balkans dating back to the 1870s, and malevolent Germans and the navy they began building in 1897. A contemporary version of this fallacy traces the 9/11 attacks back to the Egyptian government’s 1966 execution of Sayyid Qutb, the Islamist writer who inspired the Muslim Brotherhood. Most recently, the financial crisis that began in 2007 has been attributed to measures of financial deregulation taken in the United States in the 1980s.

Ferguson proclaims that the real truth is found in the opposite direction:

In reality, the proximate triggers of a crisis are often sufficient to explain the sudden shift from a good equilibrium to a bad mess. Thus, World War I was actually caused by a series of diplomatic miscalculations in the summer of 1914, the real origins of 9/11 lie in the politics of Saudi Arabia in the 1990s, and the financial crisis was principally due to errors in monetary policy by the U.S. Federal Reserve and to China’s rapid accumulation of dollar reserves after 2001. Most of the fat-tail phenomena that historians study are not the climaxes of prolonged and deterministic story lines; instead, they represent perturbations, and sometimes the complete breakdowns, of complex systems.

I’m going to quibble with the Laurence A. Tisch Professor of History here.

Even if you’re a very-well-informed individual, I bet you’ve never heard of Rudolf von Havenstein–I certainly hadn’t until I read this piece at Isegoria. (Follow the links for much more detail.)

Havenstein was a “decent, hard-working, intelligent and well-intentioned public servant” who, as president of the Reichsbank, had much control over Germany’s financial policies during WWI and in the early interwar era. These policies ultimately led to the great hyperinflation of 1922-23. Sebastian Haffner, a teenager during this era, describes what it was like:

By the end of 1922, prices had already risen to somewhere between 10 and 100X the pre-war peacetime level, and a dollar could purchase 500 marks. It was inconvenient to work with the large numbers, but life went on much as before.

But the mark now went on the rampage…the dollar shot to 20,000 marks, rested there for a short time, jumped to 40,000, paused again, and then, with small periodic fluctuations, coursed through the ten thousands and then the hundred thousands…Then suddenly, looking around we discovered that this phenomenon had devastated the fabric of our daily lives.