In the past I, like many general investors, shied away from the concept of market timing. It was viewed as too difficult, and many investors left the markets when stocks went down and then missed the rally on the way up, essentially “buying high and selling low”. Instead, investors were advised to “stay the course” and keep investing, assuming that, over time, the rising markets would reward continuous faith with high returns.

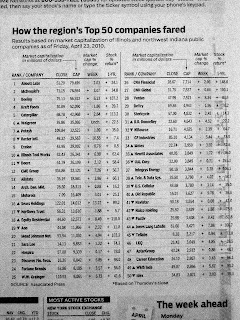

An article in Sunday’s Chicago Tribune showed in a crystal clear fashion that, in fact, market timing is the ONLY issue for stocks, at least nowadays. This article shows stock performance for the top 50 stocks by market capitalization based in the Chicago region.

EVERY SINGLE STOCK is showing positive performance over the last 12 months! What are the odds of that, assuming that the stock market has its ebbs and flows? Very remote. The ONLY issue in the market over the last few years has been timing; everyone lost in late 2008 when the market cratered, and everyone who bought in at the trough made a lot of money. Likely to see this same article in late 2008 virtually 100% of the top 50 firms would be in negative territory over the prior year.

While I can’t say for certain what is driving stock performance UP (now) or DOWN (2008), I can say that virtually the entire market is extremely correlated with this phenomenon, as indicated by the top 50 stocks all being in positive territory.

Recent articles I have seen point to returns as being closely tied to the P/E level; when you buy into a “cheap” P/E market, you do well; when you buy into an “expensive” P/E market, you do poorly. While no one can say for certain what cheap or expensive really means, that broad theory is one that might be crucial to stock investing post 2000. In modern history (the last 30 years) there hasn’t been a long period where stocks traded in such a narrow range (around the Dow 10,000 level); but we need to decide how to weight the last few decades against the entire history of the stock market.

While I am not a professional stock adviser, the fact that 50 out of 50 of the top Chicago stocks (by market capitalization) are all up has to be a signal of some sort.

Cross posted at LITGM and Trust Funds for Kids